Getting the Credit You Deserve

So, we're all worried about point size. Is it 6pt? 8pt? Adjacent to the photo? In the gutter of the page? Maybe you're a major contributor to the piece, photo-centric as some say, and so you get a big "Photographs by..." right under the title of the article. Maybe some designer somewhere has deigned your attribution to page 365 of the magazine, in a small box where no one will ever see it, yet they think nothing of giving the author a plug at the end of the article "Jane Doe previously write for this magazine on the subject of X, Y and Z in the December 2006 issue. She can be reached via e-mail at Jane@JaneDoe.com". Why the hell don't we get the same consideration?

Wait, I got off on a bit of a rant there. This piece isn't about photo credit, it's about credit, as in, I will loan you money if you pay me back more than I gave you. THAT kind of credit.

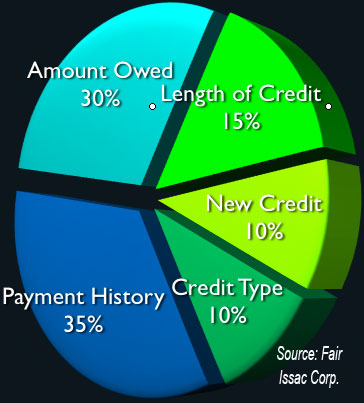

On a loan of $125,000, according to our friends at Freddie Mac, a 7% interest rate for good girls and boys means you pay a monthy combined total for principal and interest of $831.63. Bad girls and bad boys, you have a 12% interest rate, and pay $1,285.77. That means you're paying $454.14 and a total of an additional $163,490 over the life of the 30 year mortgage. Man, that sucks! So, just how do these sharks calculate what your percentage rate is? Well, the higher the risk you won't pay them back, the higher the interest rate. The folks at Fair Issac Corporation (FICO) are in charge of your future.

So, just how do these sharks calculate what your percentage rate is? Well, the higher the risk you won't pay them back, the higher the interest rate. The folks at Fair Issac Corporation (FICO) are in charge of your future.

So, what is your credit score? If the end result of between 500~579, you suck. You've not paid your bills on time. You, sir or madam, are a bad credit risk. If you're in the 760~850 range, you're golden. A perfect risk. To find out, our dear friends in the federal government have deemed it necessary for you to get one free credit report, every year. How? check out www.AnnualCreditReport.com to learn more. There are three credit bureaus that have got your number, they are Equifax, Experian, and TransUnion.

Once you've got your number, here are a few suggestions:

- You need to have credit cards. Creditors don't like people who keep cash in their mattress, they like you to play in their sandbox awhile with other people's money before they will loan you theirs at a good rate.

- Don't max out your cards. Get two, and rack them up only half way. They like this better than maxing out.

- Have a good mix. Those student loans, a car loan, and a few credit cards look better to them.

- A big paycheck doesn't mean a good credit rating.

- Be a timely bill payer. Set up your cards to be paid automatically from your bank account so you don't forget.

If you have been a bad boy or girl in the past, but are on the straight and narrow now, potential new creditors like that. More weight is given to recent credit entries in your history with the bureaus than older bad listings. Bills such as your cell phone bill can also affect your credit rating if you pay it late, and if you try to open a line of credit at a camera store, a bad credit score will preclude that.

Once you've paid your bills on time, and have good credit, then go on and worry about the point size of your photo credit, and whether or not the magazine will print your photo credit as your URL instead. (and have you tried that?)

Please post your comments by clicking the link below. If you've got questions, please pose them in our Photo Business Forum Flickr Group Discussion Threads.

9 comments:

I use my Chase Platinum Visa and actually i meant to max it out and pay it off in full. Now i hear that carrying a balance is better. Why is it so? Would you, please, explaine? Doesn't it mean that i start paying interest which can take me to debt in the long run?

I like that you bring up something so important to photographers and photography that most people (and by people I mean universities) never touch at the detriment to our profession. Money is important. Making the money you deserve and keeping the money you make is not something to take lightly. I appreciate this forum for that.

I do disagree with you on the credit card issue. I understand that you are writing on how to improve your FICO score and that is a way of doing it if done correctly. The problem is that line of thinking is the gateway drug for too many people to get into TOO much trouble. Not all mortgage loans are based only on your FICO score. You can still find people who will manually underwrite your loan and look at you as an individual.

I have seen too many photographers get into credit card debt early and just stay that way. There is a pervasive culture among us to think that we don't make much and have to live that way. I disagree.

Cash is still king and when you budget correctly, everything from cameras to cars can be purchased with it and nothing else. So for the poster "Credit Card Holder", don't do anything foolish with your credit card.

For a great book on debunking the myths of living on the FICO score and credit, pick up "The Total Money Makeover" by Dave Ramsey. It is an eye opener for all of us who have grown up nurtured by Visa, Master Card and American Excess.

I have three cards. Two for the business : an American Express and a business Visa. Every business expense goes on the American Express and only on Visa if the company (I travel quite a bit) does not accept American Express. I float huge production expenses via AMX and it helps keep everything tidy and in order for my accountant. Personal items go on my Master Card.

I registered my business as an LLC and I keep business and personal accounts at my bank. The large sums via the credit cards still count toward my credit score (which is in the 700's) and I am paying off a business loan for a medium format digital back, all of which raises my score. Automatic payments on the loan.

Besides John's excellent book, APA National (http://www.apanational.com) has some excellent papers you can download from their site that can help you with your business.

Strongly suggest to all that they attend any of the APA business seminars.

Keeping your act together with billing software is a good way to go. Some people use Quickbooks for everything, others use Quickbooks for the second half of the process.

The two gold standards for ease of use and up-to-date invoicing programs for photographers are: BlinkBid (http://www.blinkbid.com) and FotoBiz (http://www.fotobiz.net).

They are both excellent programs. I switched after many years of anquish from InView/Stock view to BlinkBid and love the program. Written by a working Los Angeles shooter, it is well thought-out and clearly presented.

Hope this helps.

Great topic by the way.

We got rid of all of our household credit cards (alright, we payed off MY credit cards) years ago, and have never looked back. I understand the idea that we "should" borrow some money now so we can borrow more money later, but it doesn't "feel" right to get credit cards for that reason alone.

To me, it has a cyclical racketeering feel to it. I am not a conspiracy theorist by any stretch of the imagination, but having the credit world dictate that the best way to get a good rating with THEM is to borrow more money, well....I think there were some legbreakers back in Jersey that had a similar business plan.

Now, the idea of getting a card, buying a new supercomputer and paying it off over the subsequent months is a VERY attractive prospect....perhaps that is why credit cards are not a good idea for me. ;)

If unsecured credit cards are not an option for you, then secured credit cards are a great way to begin rebuilding your credit. Secured credit cards require that you put a deposit into a saving account as collateral against the balance of the card. You can even get cards if you need bad credit loans.

This site contains a very good information, and here is another similar site which is having related information,for more log on to the websiteBad Credit

Having bad credit may seem like the end of the world. Because of a negative credit rating, you may be turned down for personal loans, credit cards, auto loans, and mortgages. On some conditions, bad credit loans are now easily provided by the lenders. You can use bad credit loans for any purpose such as renovation of home, purchasing a new or old car, planning a wedding party, paying for child's tuition fees, going to a holiday tour or you can consolidate debts under the loan. Or you can apply for bad credit mortgage. It will be right to say that bad credit mortgage solve two purposes: firstly, they provide financial support in fulfilling all personal and business needs and secondly, they helps in improving the credit score (if timely repayments of loan are made).

Thus, avail bad credit personal mortgages and overcome all financial hurdles being faced due to bad credit history.

As much I posible, I don't want to have a bad credit. So, I pay my bills on time and maintain my good credit. I only use my credit cards for emergency purposes only. Even for my business credit cards, which I use to finance my business, I use it at the right way. I have wrote some reviews and articles about small business credit card, you may check it on my business credit card site. Thank you for this helpful article.

asus s5000n battery

asus s5000a battery

asus s5a battery

Post a Comment